Liquity V2 Overview

Why Liquity exists, what it is and how it works

1. Why we need truly decentralized stablecoins

1.1 Counterparty risks

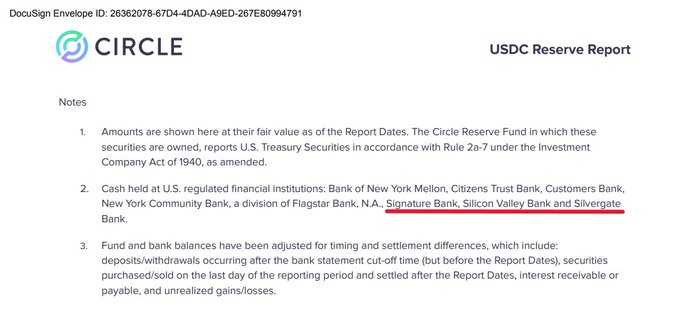

The two major stablecoins are USDT from Tether and USDC from Circle. Circle and Tether are private companies where individuals can deposit US dollar cash into their reserves to mint stablecoins.Offchain stablecoin issuers like Tether and Circle operate much like banks, with reserves in cash and bonds. External auditors audits stablecoin-issuing companies' reserves regularly (monthly for Circle). This audit verifies the composition of reserves and the organizations that hold these assets.Even though those reserves are audited, the counterparty risk still exists.

The banking crisis of 2023 exposed the fragility of centralized stablecoins when three major US banks holding Circle's reserves failed in a single week. Most critically, Silicon Valley Bank's administrative closure froze $3 billion (25%) of Circle's cash reserves, sparking market panic and causing USDC to lose its dollar peg. This wasn't unprecedented—Tether's USDT faced similar issues in 2017, though with less transparency around its treasury management.

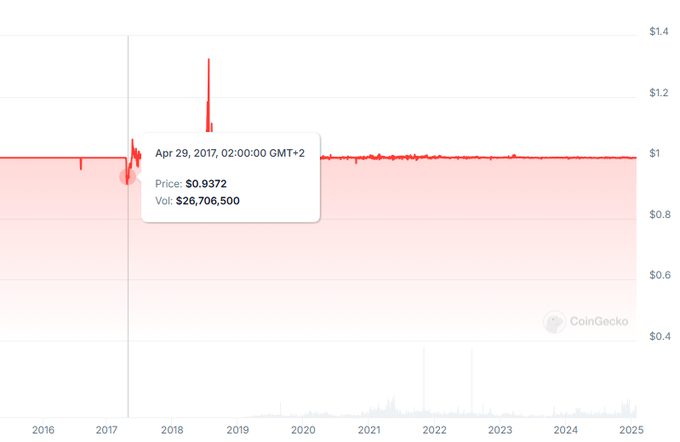

When an audit revealed that each USDT was backed by only 74 cents rather than a full dollar, it triggered a market panic and caused USDT to lose its peg. Though Tether managed to restore the peg within two weeks, the incident created lasting doubts about centralized stablecoin issuers and their role as financial intermediaries.

1.2 Censorship risks

Stablecoins issuers like Tether or Circle have a freeze function, allowing them to block transactions associated with suspected illegal activities. They have the authority to block the transfer of specific stablecoins held in specific addresses.This function is mandatory for those stablecoins issuers, as any financial institution must comply with KYC (Know Your Customer) and AML (Anti-Money Laundering) regulations. Therefore, financial institutions issuing stablecoins must comply with these rules too, and establish mechanisms to do so.

The freeze function proved useful in a recent incident involving Ledger's co-founder. When kidnappers attempted to transfer stolen USDT from the wallet, Tether froze the funds, preventing the criminals from accessing them until the freeze was lifted.

While the freeze function can stop criminal activity, it creates significant censorship risks due to unclear freezing criteria, giving stablecoin issuers arbitrary control over user transactions. This became evident in 2022 when OFAC blacklisted Tornado Cash, forcing stablecoin issuers to freeze all funds in the protocol.

Though intended to prevent North Korean money laundering, this action also blocked legitimate users who were simply seeking transaction privacy.

Moreover, the censorship threat doesn't necessarily come from OFAC, it can also come from onchain analysis companies which can blacklist wallets of people who initially had nothing to do with illicit activities.

1.3 Governance risks

The counterparty and censorship risks are well-known in the DeFi ecosystem, so it created protocols in which we can create crypto-backed stablecoins.

That said, a stablecoin issuer being onchain is not a reason to call it decentralized. Onchain stablecoin issuers also face centralization risks.

MakerDAO / Sky is heavily exposed to USDC, tokenized T-bills which have a high counterparty risk, and also exposed to other DeFi protocols like Morpho. A failure on these intermediaries could hit the DAI / USDS peg. When USDC depegged, DAI depegged as well because more than the half of total DAI supply was minted out of USDC at that time.

Those problems can become way more serious, especially Angle Protocol, with a decision from the team that was detrimental to the protocol. Angle Protocol was exposed to Euler Finance V1 with $17.6 million in USDC (around 40% TVL) deposited into it. In March 2023, Euler Finance was hacked, and lost that amount. This loss caused agEUR, Angle's Euro-pegged stablecoin, to depeg harshly.

Onchain stablecoin issuers suffered from governance risks and questionable risk management. So being onchain is not enough to be decentralized, we also need the protocol to be resilient with appropriate management.

1.4 Revenue internalization

Centralized stablecoin issuers internalize all their revenues. Circle for example, has currently $60 billions in its reserve, with 12% cash and the remaining 88% US Treasury bonds (maturing within 6 months).

For a 4.2% yield/year on those bonds, Circle gets $2.24 billion annualized revenues just with bonds yields for Circle. On the Tether side, net profits are even higher with

$3.96 billion revenues just with U.S. Treasury Bills in Q4 2024.

To compete with these players, a new trend emerged for onchain stablecoin issuers: offering revenues for users, and there are lots of examples recently:

- MakerDAO with sDAI

- Aave with stkGHO

- Ethena with sUSDe

Stablecoin issuers are creating their own “savings account” for a competitive advantage over stablecoin issuing companies. Still, they are not all equal in terms of risk management:

- sDAI is subsidized by MakerDAO's treasury, and these yields can make expenses exceed revenues.

- sUSDe rely on lots of external dependencies like Real-World Assets or centralized exchanges, leading them to have the same problems as banks.

In short, we have to bring revenues for users with a reasonable risk/reward ratio.For all those problems, Liquity aims to provide a real solution:

- Full onchain collateral to address the counterparty risk

- Immutable smart contracts to address the censorship risk

- Minimal influence of the LQTY token to address the governance risk

- Bring revenues back to users

2. Liquity V2’s BOLD Core features

Liquity V2 has chosen to focus on maximum security and maximum decentralization of its protocol. This led to a number of compromises but also to features that are unique to Liquity:

- Collateralized by ETH and liquid staked only

- User-set interest rates

- Redemption system in parallel with liquidation mechanisms

- Immutable smart contracts

- Multiple front-end implementation

2.1 Collateralized by ETH and Liquid staked ETH only

Liquity V2 made a deliberate choice to accept only three types of collateral—ETH and two liquid staking tokens (Lido's stETH and Rocketpool's rETH)—because these assets exist fully onchain, eliminating counterparty risks from off-chain collateral, and are the most actively traded assets onchain, making their prices resistant to manipulation during redemptions or liquidations.

2.2 User-set interest rates

User-ser interest rates are the main innovation in Liquity V2. When it comes to establish interest rates on a blockchain, several solutions have been created :

- Setup an onchain governance to decide how much will it cost to mint stablecoins

- Automated interest rate management with algorithms

And Liquity V2 created a new category called “user-set interest rates” where the users manage their interest rates themselves.

Every single user can choose if he wants to pay 0.5%/year in interest to mint BOLD, or pay 25%/year.

Users can change interest rates anytime. They can change them for free every 7 days, yet when changing before that time limit, an upfront fee corresponding to 7-day average interest is applied.

If users don’t feel okay with managing interest rates, Liquity V2 provides automated interest rate management options: Summerstone protocol, which adjusts rates automatically based on user-selected risk levels and protocol metrics, and Custom Delegate, where users can authorize others to manage their rates for a fee taken from either total interest or rate changes.

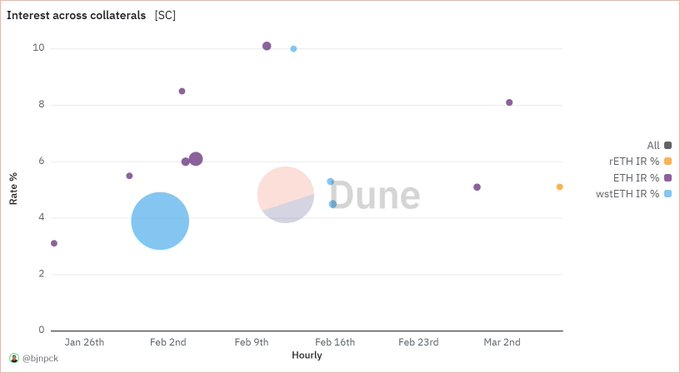

The point about letting users borrow on their own terms is disintermediation of interest rates, because in any other onchain stablecoin issuer, we have to trust something:

- In MakerDAO / Sky, we have to trust an onchain governance for interest rate management, which have difficulties to have an efficient one

- In crvUSD, we have to trust a technical intermediary, potentially vulnerable to poor upstream parameterization, or exploits.

In Liquity V2, users are fully responsible for their chosen interest rates, so the interest management is purely market-driven.

2.3 Peg protection mechanisms

An onchain stablecoin issuer must follow the average market interest rate. If the interest rate is too low, users will make carry trades, hence creating excessive selling pressure for the stablecoin resulting in depeg below $1. Lots of stablecoin issuers suffered from carry trades because of lower interest rates than the average.

Now, we have a protocol allowing users to set the interest rates they want, without any intermediary. Since users put their own interests first, Liquity V2 had to find mechanisms in order to incentivize users for protecting the peg.

2.3.1 Redemptions

Where most of stablecoin issuers rely solely on a liquidation threshold, Liquity V2 introduces a redemption system, taken directly from V1’s. But unlike V1 where redemption was based on the collateralization ratio (which poses serious problems of capital efficiency), Liquity V2 is based on the interest rates.

How the redemption system works: The peg protection system looks like a "ticking bomb" circulating between all users who have issued BOLD, and the users with the lowest interest rates are holding the bomb:

- When BOLD is trading at around $1 on the external market, nothing happens.

- When BOLD is trading at a price inferior to $1, the redemption system is activated (see below)

The redemption system allows users to exchange BOLD for collateral by targeting borrowers with the lowest interest rates. Redeemers pay off these borrowers' debt and receive equivalent collateral in return. The affected borrowers keep their net value but have reduced ETH exposure. A dynamic redemption fee (starting at 0.5%) is paid by redeemers to borrowers and helps prevent price manipulation.

Redemptions become profitable when BOLD trades below $0.995 (or less depending of the dynamic redemption fee). This mechanism encourages borrowers to set competitive interest rates, as rates too low risk redemption while rates too high cost more than necessary, helping maintain BOLD's dollar peg.

In the case where two users have the same interest rates on redemptions, the user with the most recent rate (by minting BOLD or rate change) is redeemed first.

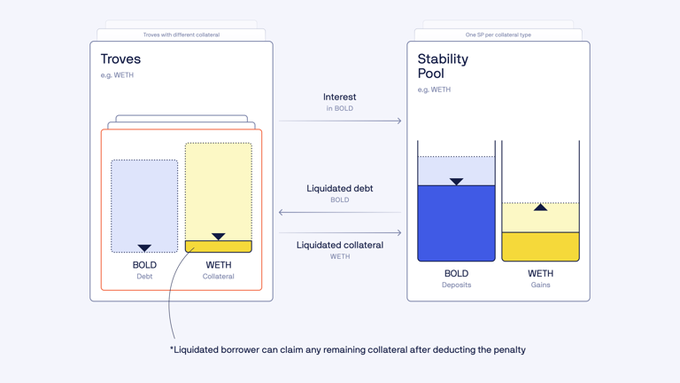

2.3.2 Liquidations

The redemption system is a thing, but we still want to have at least $1 of collateral for $1 of BOLD paid back, so Liquity V2 also has a liquidation threshold.

If a borrower's Loan-to-Value (LTV = Borrowed Assets / Collateral Assets) ratio gets above a given threshold, it is liquidated. This threshold is relative to the borrower’s collateral type:

- 90.91% LTV ratio for ETH (or 110% collateral ratio)

- 83.33% LTV for liquid staked ETH (or 120% collateral ratio)

Unlike the redemption system, liquidation implies a net loss for the borrower with different penalties according to the scenarios described below

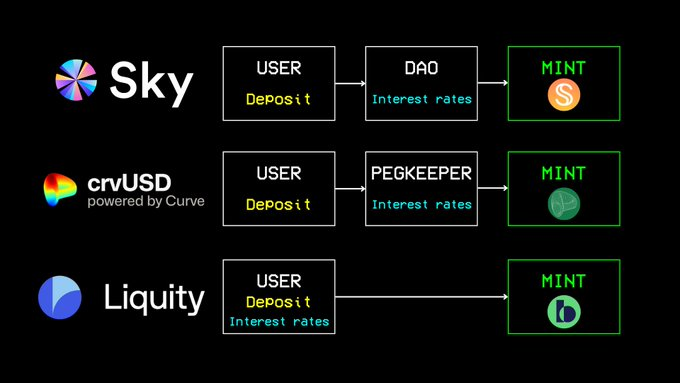

So Liquity V2 has three liquidation mechanisms to protect from bad debt:

- Stability Pool (5% penalty)

- Liquidators when the Stability Pool is empty (5% penalty)

- Redistribution when there is no liquidator and Stability Pool is empty (the user loses his entire debt and collateral. All borrowers receive a share of the remaining collateral and a debt increase, in proportion to their own collateral amounts)

3. Censorship resistance features

While onchain collateral and trustless mechanisms help make Liquity's stablecoin censorship-resistant, the protocol takes two additional steps: it uses immutable smart contracts to prevent unwanted updates, and open-sources its front-end code so anyone can run their own interface.

3.1 Immutable smart contracts

The core features of Liquity V2 are immutable, so there is no way to update the core contracts like modifying enabled collaterals, or the protocol’s mechanisms.DeFi is a landscape evolving rapidly, so building immutable contracts instead or upgradable contracts would be considered as counterproductive. That said, in the case of Liquity V2, immutability makes sense as it makes it predictable:

- Users can borrow stablecoins for years knowing the core system stays the same

- Builders can make protocols on top of it, and stays relevant over time instead of being outdated because of an update

- Lots of protocols (even stablecoin issuers) rely on multisigs with no protection mechanisms, and there were lots of compromised multisigs in DeFi history. There can't be such risks with immutability

Liquity V2 was made to be simple, predictable and protected from involuntary updates, so immutable contracts were well suited.

3.2 Multiple front-end implementation

Liquity V2 has its own front-end with Liquity.app, but the team encourages the community to run their own front-ends as it is under MIT License. MIT License allows unrestricted use, modification, distribution, and private use of the front-end, so we can build multiple front-end and have alternatives in case the official one is shut down, or censored. This though, doesn't stop other teams from creating front-ends with their own specific features, like DeFi Saver with automation features.

4. Revenues for users

As said in introduction, bring revenues for users became the new narrative adopted by onchain stablecoin issuers to make their stablecoin attractive. Every protocol has its own method to bring revenues:

- Subsidies: yields come directly from the protocol treasury. As examples, Sky spends $142 million to pay the yields (respectively $112 million/year for sUSDS and $30 million/year for sDAI), and Aave spends $20 millions/year.

- Strategies: yields come from external protocols, or offchain entities. The best example is Ethena, using delta-neutral strategies with derivative exchanges to bring yields to sUSDe.

- Economic activity: yields are directly correlated with protocol activity.

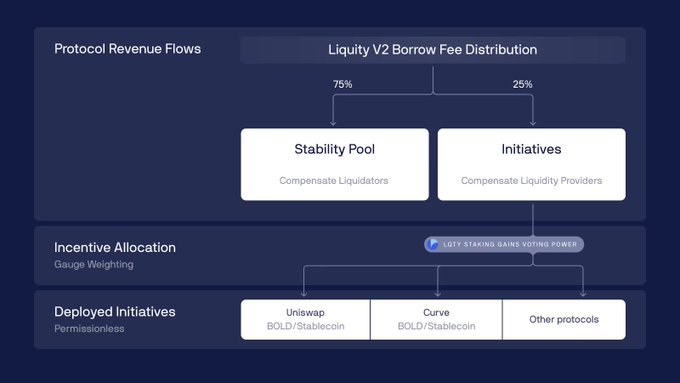

The purpose of Liquity V2 is to be as resilient as possible, with as little interdependence as possible. Therefore, the yields will come from economic activity.75% of interest paid by borrowers will be directed toward the Stability Pool, and the remaining 25% will be directed toward Protocol-incentivized liquidity.

4.1 Stability Pool

The Stability Pool is a module created to keep the protocol stable during liquidations. From a certain point of view, Stability Pool can be described as an insurance fund, as this is the first line of defense to protect against bad debt.

Bad debt: debt without collateral available to repay it. It can happen that some positions on a protocol are insolvent. If the bad debt is too high, the protocol risks dying.

The BOLD stablecoins contained into the stability pool are used to pay back liquidated borrower’s debt in return for collateral. Each collateral type (ETH, stETH and rETH) has its own Stability Pool, so depositors can choose which collateral type they wish to act as guarantor.

So Stability Pool depositors get two sources of revenues, proportional to their stake in the pool:

- 75% of the interests paid by borrowers

- Liquidation gains from the associated collateral asset

Those revenues are not risk-free. There is always a possibility of bad debt, caused by a collateral price collapse or oracle failure. If there is bad debt in the system, BOLD from all Stability Pools could be burned pro-rata to cancel it.

Hence the fact that each type of collateral has its own stability pool: according to risk profile, some users can vouch for LSTs, while others prefer ETH.

4.2 Protocol-incentivized Liquidity (PIL)

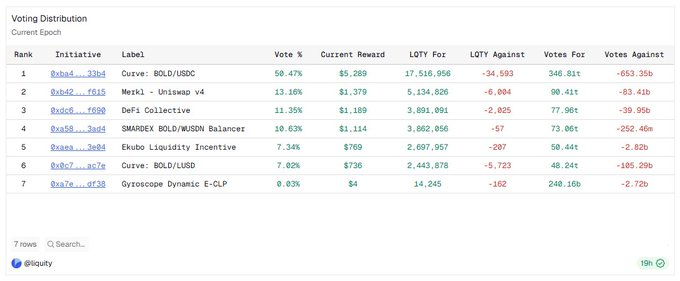

On Liquity V2, 25% of revenues paid by borrowers are collected and redirected to any onchain address, called “Liquidity initiatives”. Those liquidity initiatives can be liquidity pools (e.g. BOLD-related pools on Uniswap or Curve), rewards for lending protocols, or any address willing to participate in Liquity’s growth.

4.2.1 How to participate as a voter

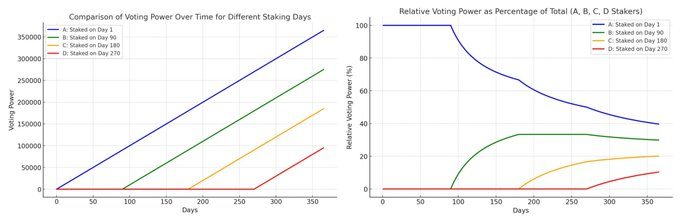

Step 1: to participate as a voter, we have to stake LQTY tokens. The longer the stake, the more stakers have voting power (users can leave anytime without penalty)

Voting Power for 100 staked LQTY:

- Day 0 = 0

- Day 1 = 100

- Day 90 = 9,000

Other examples:

- 500 LQTY (from day 0) at day 90 = 45,000

- 500 LQTY (from day 0) + 100 LQTY (from day 40) at day 90 = 50,000

⚠️When reducing you stake, your voting power is reduced proportionally, whatever the number of stakes and their respective age. In other words, we can't choose LQTY with a specific age to withdraw.

- Initial stake = 500 LQTY (from day 0) + 100 LQTY (from day 40)

- Withdraw 50%

- New stake = 250 LQTY (from day 0) + 50 LQTY (from day 40)

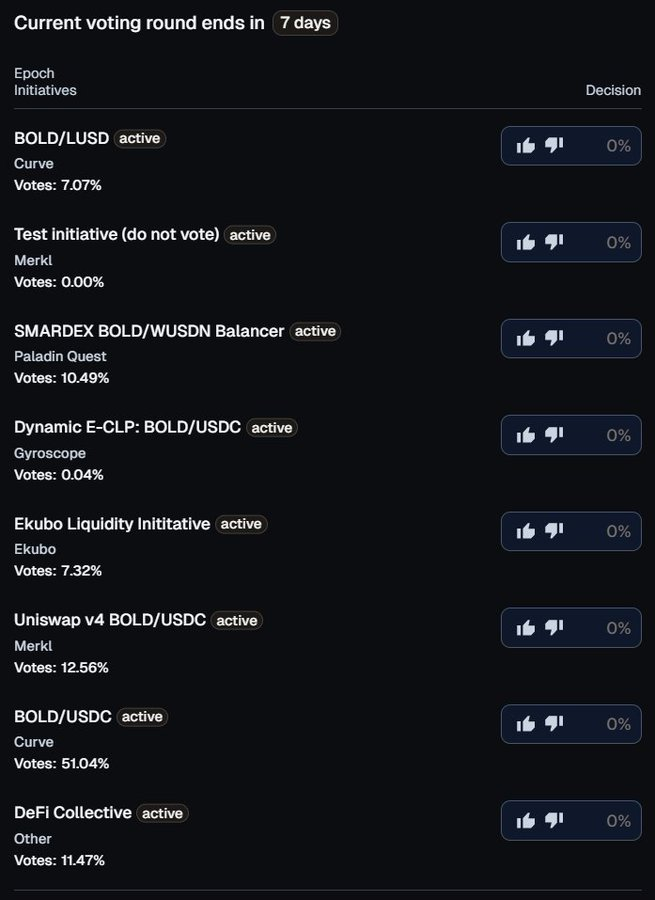

Step 2: LQTY Stakers can vote or downvote (“veto”) initiatives by giving any percentage of their voting power. Vetoes don't count for incentives. However, if vetoes > votes, the initiative is unregistered.

Step 3: The voting periods (called "epochs") start from Thursday (00:00 UTC) to the following Wednesday (23:59:59 UTC). Votes are disabled 24 hours before the end of the epoch and only vetos are available, to avoid last-minute changes or malicious initiatives.

Step 4: Once a user votes, the distribution of votes and vetoes will be saved for future epochs, until users wish to change it.

4.2.2 How to participate as a liquidity initiative

Step 1: Initiatives are permissionless but have a cost. To do so, the proposer must hold at least 0.01% of all voting power and pay a registration fee of 1000 BOLD. These measures have been adopted to prevent spam

Liquity has a forum where incentives are proposed and discussions around them happen. This is a good place to take the temperature on the proposed initiative, and if it's relevant enough, it can be supported by other stakeholders.

Step 2: Any Ethereum address can receive PIL, but the team recommends to create a smart contract containing any logic necessary to direct any received funds in BOLD.

Step 3: Let's assume that the initiative is eligible for voting. It must reach at least 2% of total votes to qualify for incentives, but they must hurry: Initiatives failing to reach this threshold during four consecutive epochs may be unregistered.

Step 4: at the end of an epoch, all initiatives with at least 2% of total votes get the Protocol-Incentivized Liquidity (PIL), split in proportion to the relative votes (see above).

Example with 10,000 BOLD as PIL:

- First initiative (50% vote, 0% veto) = 7,700 BOLD (77% relative votes)

- Second initiative (10% votes, 20% veto) = 0 (vetoed)

- Third initiative (15% vote, 4% veto) = 2,300 BOLD (23% relative votes)

- Fourth initiative (1% vote, 0% veto) = 0 (under 2%)

Beware of sleeping on incentives! They must be claimed in the same week, else they get redistributed to the next epoch. Furthermore, if the weekly claim is not done for more than four consecutive epochs, an initiative can be unregistered.

Bribes: Bribes are payments made by third parties to influence how LQTY stakers vote on PIL allocations (spend x amount as bribe, hoping to get more than x as PIL rewards)

Bribes are permissionless, so no need for any approval to bring incentives for any initiativeLiquity has provided open source Bribe adapters that can be extended and modified by developers.

5. Friendly forks

As previously stated, Liquidity V2 is an immutable stablecoin issuer, and the only eligible collaterals are ETH, stETH from Lido and Rocketpool, and it’s gonna be this way until the protocol is exploited or Ethereum is shut down. But what if users wanted to borrow stablecoins against other tokens? Or add features like integrating other protocols?

This is possible by building a “friendly fork” of Liquity V2. A “friendly fork” is a protocol copying some of Liquity V2’s source code, and approved by the core team as the source code is under Business Source License (BUSL) until September 1st, 2027.

The core team’s approval is necessary to build a fork during that time. In return, a friendly fork benefits from the network effects and incentives from the landscape that is Liquity V2’s shared codebase. Before going anywhere, let's take a look at what BUSL is all about, and why it matters for Liquity V2.

5.1 Liquity V2 is under BUSL

Concretely, software under the BUSL (Business Source License) makes the source code available to any user, who can view the code and use it for non-commercial purposes.

Nevertheless, once the software’s code is made publicly available, there is a time period (typically lasting several years) during which commercial use is restricted.

These restrictions can be directly specified by the development team behind the project—meaning some features may be freely usable, but not all. It is also possible to require a commercial license, obtainable through payment (or other agreed-upon terms between stakeholders), without which commercial replication of the code is prohibited.

Once this time period expires, these restrictions are lifted, and the software officially becomes Open Source (under a license of choice, such as MIT, Apache, or GPL). This allows the development team to be "compensated upfront" for their proposed project.

In the blockchain industry, the first project to adopt the BSL was Uniswap V3, for a duration of two years. Since 2023, Uniswap V3 is Open Source software under the GPL 2.0 license, and many DeFi protocols use them as well like Uniswap V4, Aave V3, Eigenlayer and as we might expect, Liquity V2 is among them.

5.2 Why BUSL?

Since its introduction in 2021, the BUSL license has been a particularly controversial topic in the DeFi community. The debate continues to this day, and could be the subject of another article.

The team choose to put Liquity V2 under license, mainly because of the past experience they had about Liquity V1 forks.

To date, Liquity V1 has been forked 39 times. The vast majority of these forks were deployed without prior communication with Liquity, and without any willingness to cooperate.

In other words, they wanted to “vampire” Liquity instead of building something new. And this was detrimental to users, because on the one hand Liquity was fragmented, and on the other certain security standards were not respected.

Among Liquity V1's 39 forks, only Gravita Protocol chose to collaborate with the team, contributing innovations like LST integration. This experience led Liquity to adopt the BUSL license, which encourages developers to create "friendly forks" that build upon the protocol cooperatively rather than competitively.

5.3 Synergies with forks

By collaboration, we mean that the friendly forks will cooperate with Liquity in several ways, the first one is obviously bringing new features to the original protocol possibilities:

- More tokens as collateral, each fork having its speciality. DeFiDollar is focused on DeFi tokens (AAVE, CRV, UNI…), while others like Felix is focused on the Hyperliquid ecosystem with HYPE

- Protocol integrations like Nerite integrating Superfluid for streamable stablecoins

- Although the original protocol is immutable, some forks can choose to have upgradable contracts and have adjustable risk parameters, or updates.

Liquity and its friendly forks create a mutually beneficial liquidity system. Each fork must incentivize BOLD liquidity pools on Layer 2s and mainnet, typically allocating 4% of their token supply as rewards. Meanwhile, LQTY stakers can direct 25% of Liquity V2's revenues to support fork liquidity.

This creates a positive feedback loop—more forks lead to more stablecoin minting, generating more protocol revenue and incentives. In this way, Liquity serves as a development framework for stablecoins, similar to how Optimism's OP Stack supports rollup development.

6. Risks and tradeoffs

Liquity has always kept the same goal in mind: to create the most decentralized stablecoin issuer possible on Ethereum, with the fewest external dependencies. To achieve this goal, Liquity has had to adopt a number of compromises that may either limit the growth of this stablecoin, or constitute a potential risk.

Even though Liquity takes every possible precaution, the protoco is not free from potential bugs or other technical risks, especially given what happened last February.

6.1 Technical risks

The protocol has been through many audits. Security has always been a major concern for the team, and this is all the more important when the smart contracts deployed are immutable. This didn't prevent finding a vulnerability in the Liquity V2 code when the protocol was first deployed.

On February 12th 2025, the Liquity team was informed of a potential issue affecting Liquity V2 Stability Pools. This issue has been confirmed the day after, Stability pool depositors had to close their positions as soon as possible and borrowers were advised to close their loans while BOLD liquidity remained favorable.

This misadventure had a happy ending after all: no funds loss were reported so far, and only Stability Pool was impacted while every other part of the system was intact. That said, the contracts were immutable, the only way to fix the issue is to redeploy a patched version Liquity V2, and the first deployment will become a legacy protocol.

The Liquity team must be praised for its transparent communication on the vulnerability, and for ensuring that no user loses funds. However, this is also a reminder that there is no such thing as zero risk in DeFi.

6.2 Bad debt risks

We mentioned above the bad debt risks, and in this section we will look at how they can arise and the measures we can take to protect ourselves against them:

- The collateral price can collapse in case of massive liquidations or liquid staking token depeg.

- Oracle failure can bring the collateral price up or down. Downward price can bring the underlying collateral at a value under $1, leading to bad debt, while upward price overvalues collateral, leading to excessive BOLD minting destabilizing the system.

In the event of bad debt, here are five of the main measures put in place:

- When bad debt exists, direct normal redemption fees to clearing the bad debt

- Haircut for Stability Pool depositors. As said before, depositors vouch for BOLD peg if redemptions are insufficient.

- Socializing the loss across existing Troves.

- New multi-collateral Stability Pool to absorb some fraction of liquidations, including collaterals with bad debt.

- Use Protocol Incentivized Liquidity to clear bad debt. It could be proposed just like any other liquidity initiative.

6.3 Protocol-Incentivized Liquidity disruption

25% of the interest paid by users for issuing stablecoins is accumulated and distributed on a weekly basis. Under normal circumstances, these funds should be used to support Liquity's growth, and token holders have a financial interest in participating in this growth.

In a scenario where Liquity V2 is a resounding success, the prospect of obtaining 25% of its revenues would be tempting for many users who would try to present liquidity initiatives to be used not for liquity's growth, but for their own purposes.

This is a risk because DeFi protocols like Compound have already been exploited with governance attacks. In July 2024, a group known as the “Golden Boys” submitted "Proposal 289: Trust Setup for DAO Investment into GoldCOMP" which aimed to transfer 499,000 COMP tokens (5% of the treasury, valued at significant millions) to an unmonitored multisig wallet under their control. That attack was possible because of low voting participation, and 1 token = 1 vote.

Concerning Liquity’s voting system, there are safeguards to prevent this governance attack from happening:

- Raw voting power is accruing over time

- LQTY onchain liquidity is low

- Malicious liquidity initiatives can be vetoed

On the other hand, the system will tend to favor long-standing stakers with large amounts of staked LQTY, so the total staked LQTY must be as high as possible to dilute relative voting power.

6.4 Growth ceiling

Liquity V2 boasts major growth levers as the entirety of interests paid by users are redistributed to other users (75% to stability pools, 25% to PIL). Consequently, there can’t be value capture from this kind of intermediary, so more incentives to make BOLD competitive.

Although this revenue sharing confers important possibilities, its influence is highly dependent on the revenues generated by Liquity V2. Massive revenues enable massive incentives for growth potential, but zero revenues means zero incentives as well.

6.5 The friendly forks

In decentralized finance, we often have to strike a balance between predictability and evolution. A conservative system is predictable yet closed to any evolution, whereas an evolutive system can bring innovations yet can be unstable, even dangerous.

The Liquity team decided to pursue both extremes. The original version of Liquity V2 will opt for the maximally conservative setting with immutable contracts and only three assets as collateral.

The maximally evolutive side will be led by the friendly forks with the features mentioned in the friendly forks section.

The teams responsible for developing friendly forks can collaborate with the Liquity team to make sure their protocol is as safe as possible. Despite that, forks are the most vulnerable to bug exploits, due to the additional features they offer.

Additionally, we have to assume 2-3 forks will concentrate at least 80% of the economic activity dedicated to them, as some will be more innovative and/or hyped than others.

Final thoughts

Liquity V2 has maintained its commitment to create a genuinely decentralized stablecoin issuer, designed to operate in all market conditions with user-set interest rates. But throughout this topic, we can realize Liquity V2 has another objective in mind: bring disintermediation within stablecoin issuers as a whole.

Looking back at the stablecoin industry in general, most of the problems faced by stablecoin issuers stem from intermediaries, starting from stablecoin issuing companies:

- The companies still represent a counterparty risk

- Current regulations for these companies impose censorship mechanisms

- Companies keep all revenues for themselves

Still, onchain stablecoin issuers also need disintermediation because they can struggle with intermediaries like onchain governance too. Governance is suboptimal for defining parameters such as interest rates, and it can be overridden.

The first stablecoin issuers were designed to imitate existing systems such as central banks. Liquity V2 is one of the projects that grasp blockchain's full potential for disintermediation, and applies it to stablecoins in the hope of solving their current problems.

Of course, the design of Liquity V2 required some tradeoffs that may limit its widespread use. That said, this stablecoin issuer is among those that come closest to the original values of decentralized finance: decentralization, disintermediation and censorship resistance.