Law issues about liquidity pools

Source : https://www.youtube.com/watch?v=g8x6ulKjnq8

Liquidity Pools

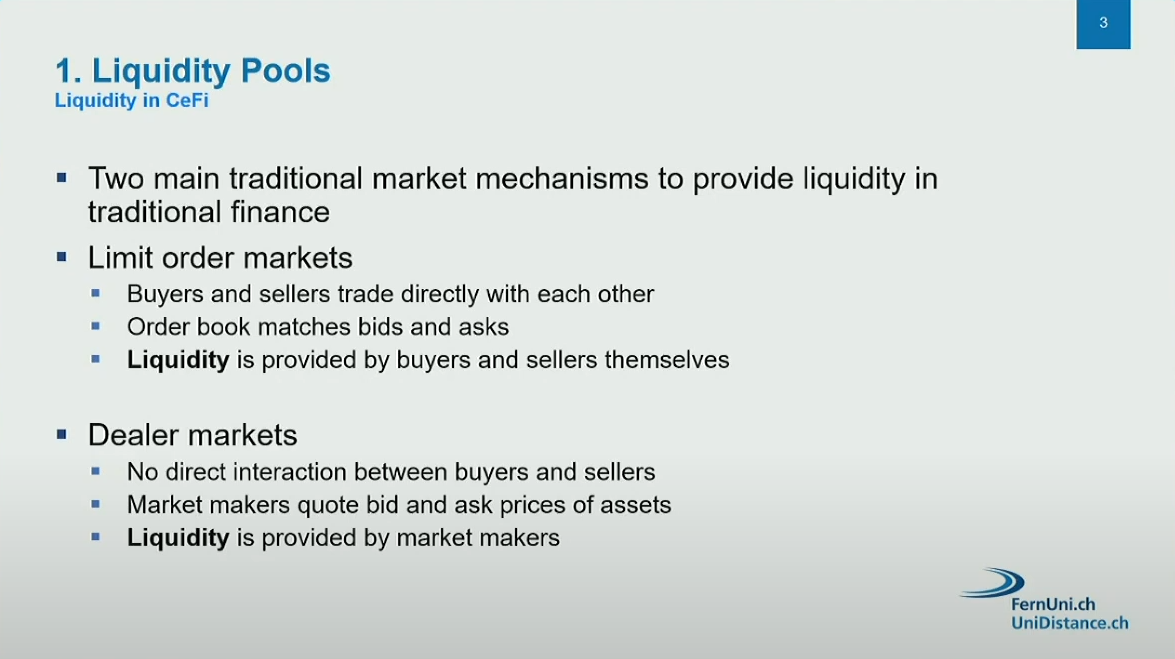

Liquidity is essential for any market, whether centralized or decentralized finance. Liquidity allows traders to execute orders without significantly affecting the price. In a perfectly liquid market, any order size can be filled at the same price.

Liquidity in CeFi (1:15)

Traditional ways to provide liquidity in centralized finance markets :

- Limit order markets

- Liquidity is provided by market participants (buyers and sellers).

- Participants place limit orders (specifying a maximum/minimum price) or market orders (no price specified).

- An order book matches bids and asks (buy and sell orders).

- Dealer markets

- Liquidity is provided by regulated market makers (brokers affiliated with exchanges).

- Market makers maintain an inventory of assets and quote bid and ask prices.

- Participants transact with market makers instead of each other.

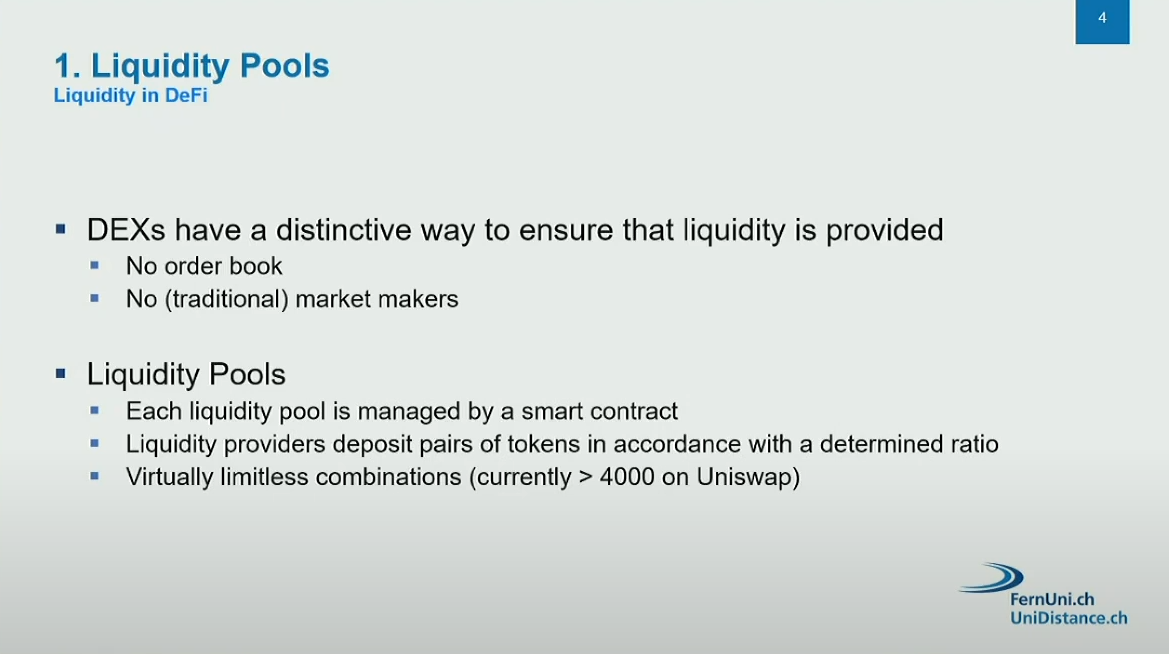

Liquidity in DeFi (3:55)

Liquidity provision in decentralized finance (DeFi) is different from traditional finance. There is no order book matching bids and asks, and no traditional market makers.

Liquidity in DeFi is provided through liquidity pools:

- Anyone can be a liquidity provider, not just professionals.

- Crypto tokens are deposited into pools managed by smart contracts.

- Prices/ratios are determined solely by the smart contracts, not external factors.

- Allows for virtually limitless combinations of token pairs (e.g., over 4000 on Uniswap).

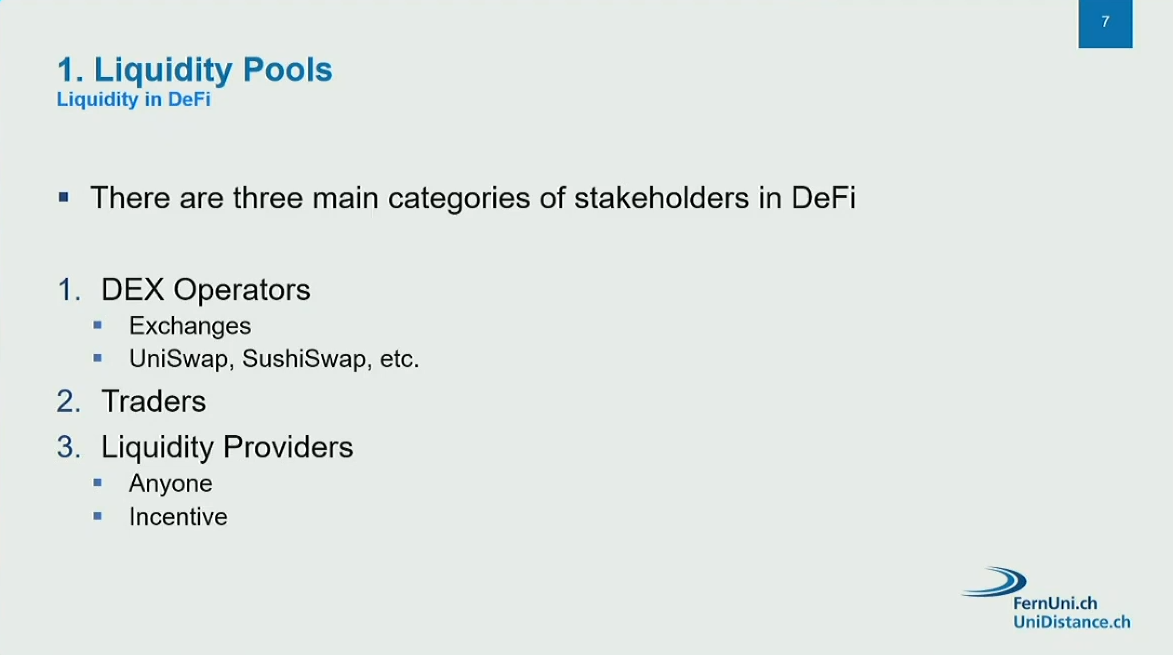

Stakeholders in liquidity pools are operators of the DeFi platforms/interfaces, traders and liquidity providers

There are difficulties identifying the legal entity/person behind the platform interface. In some cases (e.g., Uniswap), smart contracts are deployed by users, not the platform itself.

Legal relationship between stakeholders

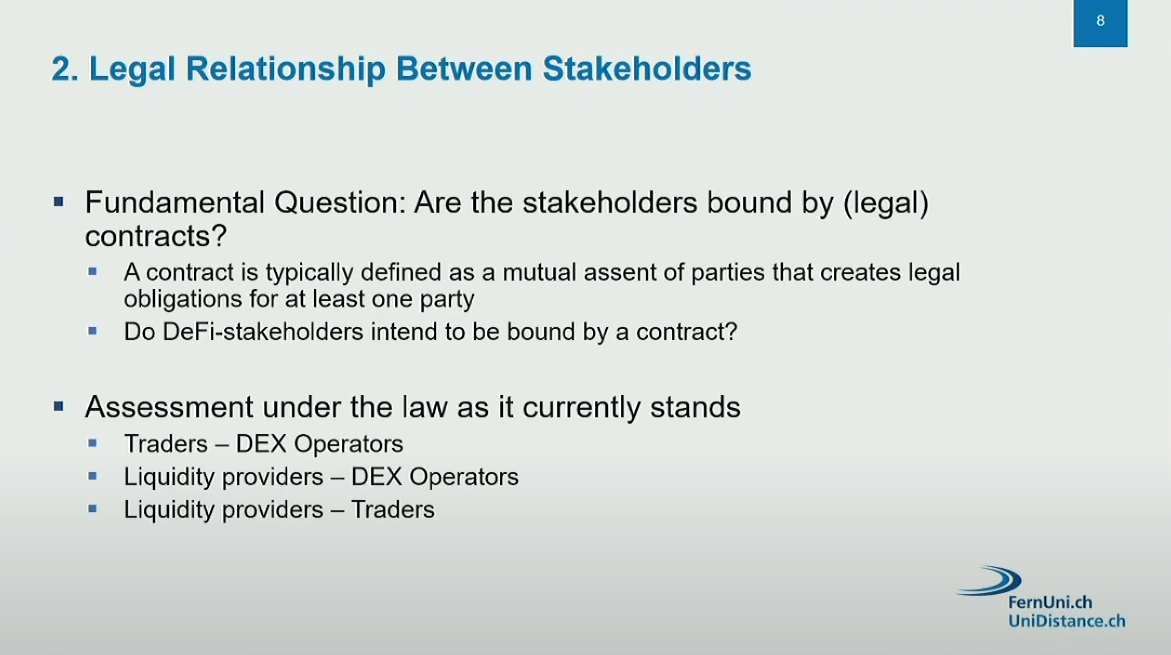

Legal relationships between stakeholders in DeFi liquidity pools

A contract requires agreement by parties to be legally bound, and it's unclear if DeFi stakeholders intend to create legal relationships.

However, terms of service on platforms like Uniswap suggest users must agree to enter legal contracts.

The actions of giving/receiving value resemble contractual obligations.

Relationship between traders and platform operators

Platforms have an obligation to provide access to the interface, and traders have an obligation to pay fees.

This could be considered a contract for work and services under Swiss law.

Relationship between liquidity providers and platform operators

Platforms must provide access to the interface, and liquidity providers are essential for the system's functioning.

Legally, liquidity providers could be considered vicarious agents needed to perform contractual obligations.

Relationship between liquidity providers and traders

Tokens are pooled, but no interaction between these actors, so liquidity providers and traders do not directly interact

Likely no legal relationship or contract exists.

Compensatory claims

Legal basis (11:10)

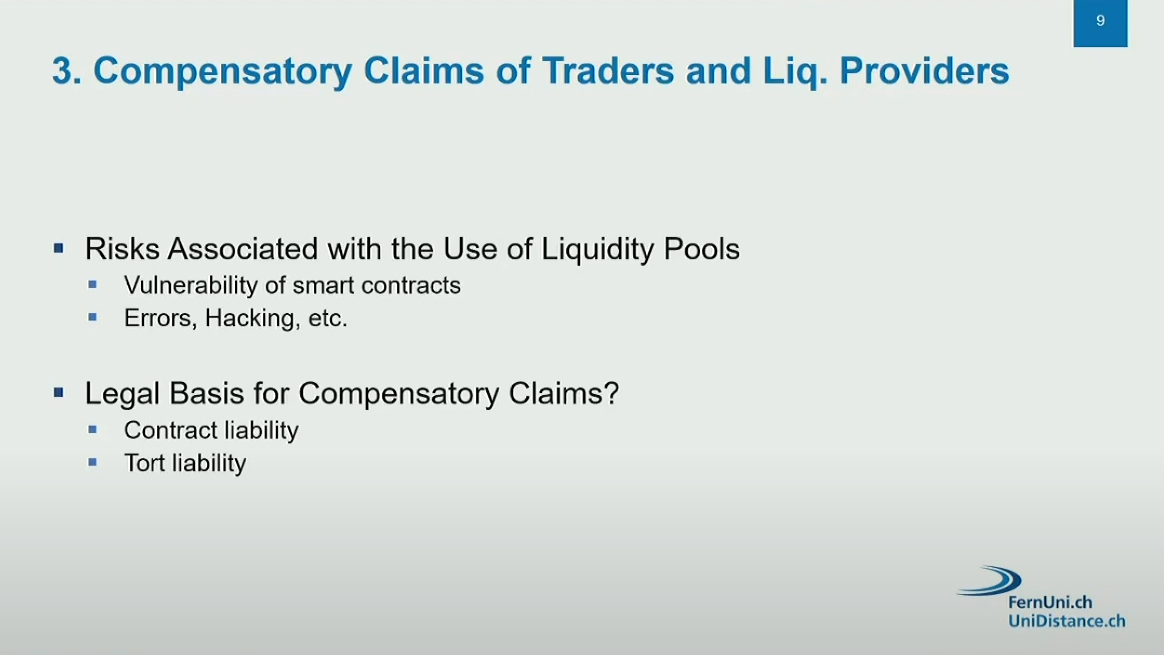

Smart contract hacks can lead to loss of funds for liquidity providers and traders.

There is a possibility of users (liquidity providers or traders) seeking compensation, likely from the DEX operator rather than the unknown hacker.

Analyzing the claims under current Swiss law (13:20)

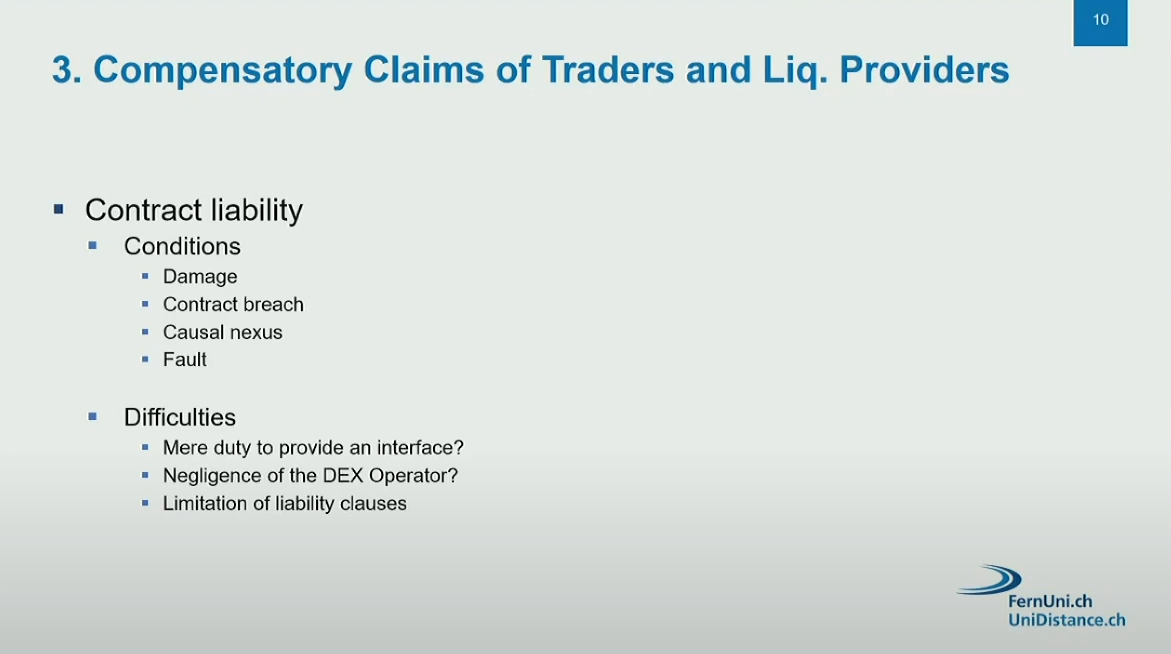

Contract liability : Fault/fraud may not be easily proven if the DEX operator tried their best, but causation between breach and damage may be possible to prove.

That's why DEX operators' terms of service often disclaim responsibility for smart contracts.

Tort liability : Similar issues in proving fault/negligence by the DEX operator.

Additional requirement of proving the DEX operator intended to steal assets (difficult unless a rug pull).

Under current Swiss law, it is very difficult for users to obtain compensation from DEX operators due to :

- Challenges in proving contractual breach or fault/negligence.

- DEX operators can limit liability in terms of service, except for gross negligence.

- Establishing causation and damages may also be complicated.

Challenges & Outlook

Overall, the current legal system is not well-suited for compensating users who lose funds due to smart contract hacks on DEXs. But there also additional challenges :

- Participants are pseudonymous or anonymous

- Transactions are irreversible

- DeFi is transnational, requiring difficult cross-border cooperation

Question : do we need and want greater protection for users ?

👿Bad option : More licensed regulation for market participants like DEX operators

😇Preferred option : Introduce strict/compulsory liability for DeFi market participants, e.g. remove fault requirement for tort liability in the DeFi ecosystem

A more suitable approach for DeFi may be to sanction certain actions/behaviors instead of focusing on participants

Can a centralized exchange or bank accept tokens that were potentially "tainted" by being routed through an AMM pool that had previously received liquidity from an illegal entity like a hacker ? (21:30)

The presentation addressed the contractual relationships between traders, liquidity providers, and DEX operators, but did not cover AML (anti-money laundering) regulations or criminal liability aspects.

In some countries, AML regulations may require centralized exchanges to have measures to prevent accepting funds from liquidity pools that were obviously derived from hacked sources or criminal activities.

The new MICA (Markets in Crypto-Assets) regulation in Europe aims to have a uniform regulatory framework, which may include obligations related to tracing the sources of funds in liquidity pools.

While there is no contractual relationship between traders and liquidity providers, that does not necessarily absolve centralized exchanges from obligations to check for and prevent facilitating criminal activities through the funds they accept.