Hypeful narratives for 2026

Non-USD stablecoins

Context

It is often said that 2025 was one of the best years for stablecoins. In fact, the biggest winner is not stablecoins per se, but the US dollar.

USD has already won at DeFi for several years, where approximately 99% of all existing stablecoins are pegged to the dollar (representing about $300 billion). When stablecoins are traded, they involve USD 99.9% of the time. So DeFi had already been conquered long ago

It is from a regulatory perspective that the USD gained the most, particularly with the passage of the GENIUS Act. Beyond the fact that this is another step towards separating money from the state, the GENIUS Act also ensures that USD comes out on top in every regard:

- Companies must replicate the Tether/Circle business model for their stablecoin. Since the US Treasury bills back 80% of stablecoins in circulation, the United States has succeeded in creating new demand for its debt

- Companies are incentivised to create their stablecoins, and some of them have already ventured into banking without saying so

- Stablecoins are accessible to anyone worldwide. There have never been so many users who own USD, even though they do not live in the US.

Stablecoins have enabled the USD to create global demand, and the GENIUS Act is designed to channel this demand towards US debt. Somehow, companies are becoming "dollar franchises", and this is why USD is the biggest winner of 2025.

Now, why being hyped about non-USD stablecoins?

First of all, there is a growing awareness in several countries that stablecoins have become a vector of globalisation. As a State, it is possible to have its debt financed by anyone around the world thanks to stablecoins.

Secondly, stablecoins can also be created to move value where banks can no longer do so reliably.

Thirdly, DeFi has more means to help the growth of non-USD stablecoins.

Finally, non-USD stablecoins also cover commodities, and we know of certain commodities that have outperformed crypto during 2025.

GENIUS Act alike

With everything happening in the US, fintechs from other countries are motivated to issue stablecoins by bank deposits and government bonds as well.

Tokyo-based fintech company JPYC has registered as a money transfer business in order to issue the JPYC stablecoin, backed by bank deposits and government bonds to maintain its parity with the yen.

Although their beginnings were modest, they set themselves the goal of issuing 1 trillion yen (approximately $6.81 billion) over three years.In 2025, Hong Kong adopted an ordinance establishing a licensing regime for stablecoins backed by currencies, starting with the Korean won. Eight banks are already working on a won-indexed stablecoin project for 2026, and South Korea's ruling party is proposing to allow companies with capital of just $360,000 to issue won-backed stablecoins.

More surprising: this licensing regime also includes yuan-backed stablecoins. This would mean companies would be able to issue yuan-backed stablecoins, and according to recent news, tech giants like Alibaba and JD.com are really interested in this.

But issuing CNY-related stablecoins also means competing with e-CNY, built by the Chinese government. Given that the e-CNY is failing to gain adoption, the Chinese government perceives this as a direct threat, which easily explains why Chinese regulators have been interfering with Hong Kong lately.

Stablecoins as a lifeline

While most countries have found stablecoins as a means of financing their own debt, others can create a stablecoin and use it for purely geopolitical reasons.

This stablecoin is A7A5, pegged to the russian ruble. And spoiler alert, it is a controversial topic.

A7A5 was indeed created to address the needs arising from capital controls imposed on Russia. The traditional Russian banking system is cut off from international circuits by sanctions.

It was necessary to find new financial circuits, and A7A5 provided a solution.

At the time of writing, there are supposedly $500 million worth of A7A5 circulating. Even though there are dozens of USD stablecoins with higher circulating supply, A7A5 is successful, considering its supply is higher than EURC's (the euro stable with the highest supply).

But this topic is controversial for some reasons. Onchain data shows ~$500 million, the vast majority of which is on Tron, and stablecoins normally require verifiable reserves.

The problem is, we have no audit about how reserves are managed, and we can't expect to have any details about it as A7A5 has been built in a context of sanctions.

Maybe A7A5 is a successful non-USD stable actively used as a financial lifeline, maybe it's a ticking bomb that will explode either because of its opacity or because of the obvious regulatory risks.

That being said, this use case, however controversial it may be, deserves to be mentioned, and it had to be a non-USD stablecoin that sets the example.

DeFi is helping

For some non-USD stablecoins, the only way to be developed is through DeFi. This applies especially to European currencies starting with euro-pegged stablecoins.

According to DeFiLlama, euro-pegged stablecoins are looking good, with circulating supply going up and several different issuers.

In reality, Europe is not taking stablecoins seriously at all:

- The biggest euro-pegged stablecoin is EURC from Circle. Quite ironic to see the biggest onchain European currency managed by an American company

- The European Central Bank wants to have its own stablecoin, and the latest reports indicate that it will be operational in 2029 at the earliest.

Creating a stablecoin project for 2029 thinking it will work is a joke, as well as being highly disrespectful to issuers like monerium that have been operating for some time.

In summary, the chances of seeing the equivalent of a GENIUS Act in Europe are close to zero, and Europe has no consideration for existing issuers. Fortunately, there is still DeFi.

In fact, DeFi has been the best way to develop EUR-pegged stablecoins:

- EURC had growth thanks to EUR/USD liquidity pools on Base for Forex

- EURCV had growth thanks to incentives on morpho, whereas nobody wanted this stablecoin beforehand

- A LiquityProtocol friendly fork is under development to create an EUR-pegged stablecoin issuer on Gnosis

For EUR, the only way to create worthwhile stablecoin issuers is through DeFi. We had several indications confirming, hoping to see a double down.

For a CHF-pegged stablecoin, DeFi is the only way to create stablecoins, but for totally different reasons.

While the European Central Bank wants its own fully-controlled stablecoin, the SNB and the Swiss Federal Council have consistently rejected the idea of issuing such a retail CBDC.

Instead, stablecoins are classified as "Value-Stable Means of Payment", meaning that the issuance of regulated stablecoins will be reserved exclusively for payment institutions. Even banks will have to create a separate legal entity to issue them.

This also includes DeFi protocols that issue stablecoins, the most well-known of which today is Frankencoin.Frankencoin is a classic CDP protocol, with notable changes:

- Anyone can propose a new asset as collateral and, after approval by the community, use it to create ZCHF.

- Liquidations are oracleless: When a position becomes risky, other users can liquidate it: an auction mechanism recovers the collateral to buy back ZCHF and manages any surplus or deficit.

With this auction system, Frankencoin guarantees that behind every ZCHF issued, there is at least 1 CHF as crypto.

So Switzerland is well-positioned to have CHF-pegged stablecoins in DeFi as well (CHF Liquity V2 fork anyone?)

However, stablecoin issuers in DeFi also have drawbacks. When launching a crypto-backed stablecoin, you're not only competing with all other stablecoin issuers, but also with all the yield-bearing stablecoins.

So we must protect the peg, maintain maximum liquidity and offer sustainable yields in order to be competitive, and this will clearly not be possible for all stablecoin issuers. USD stables have a head start for it, but non-USD stablecoins have protocols at their disposal to catch up (Fluid V2🤞, EulerSwap from Euler...)

Commodities

The primary utility of stablecoins is to hedge against market volatility. So the definition of a stablecoin isn't limited to fiat currencies, and commodities can also be considered as stablecoins.

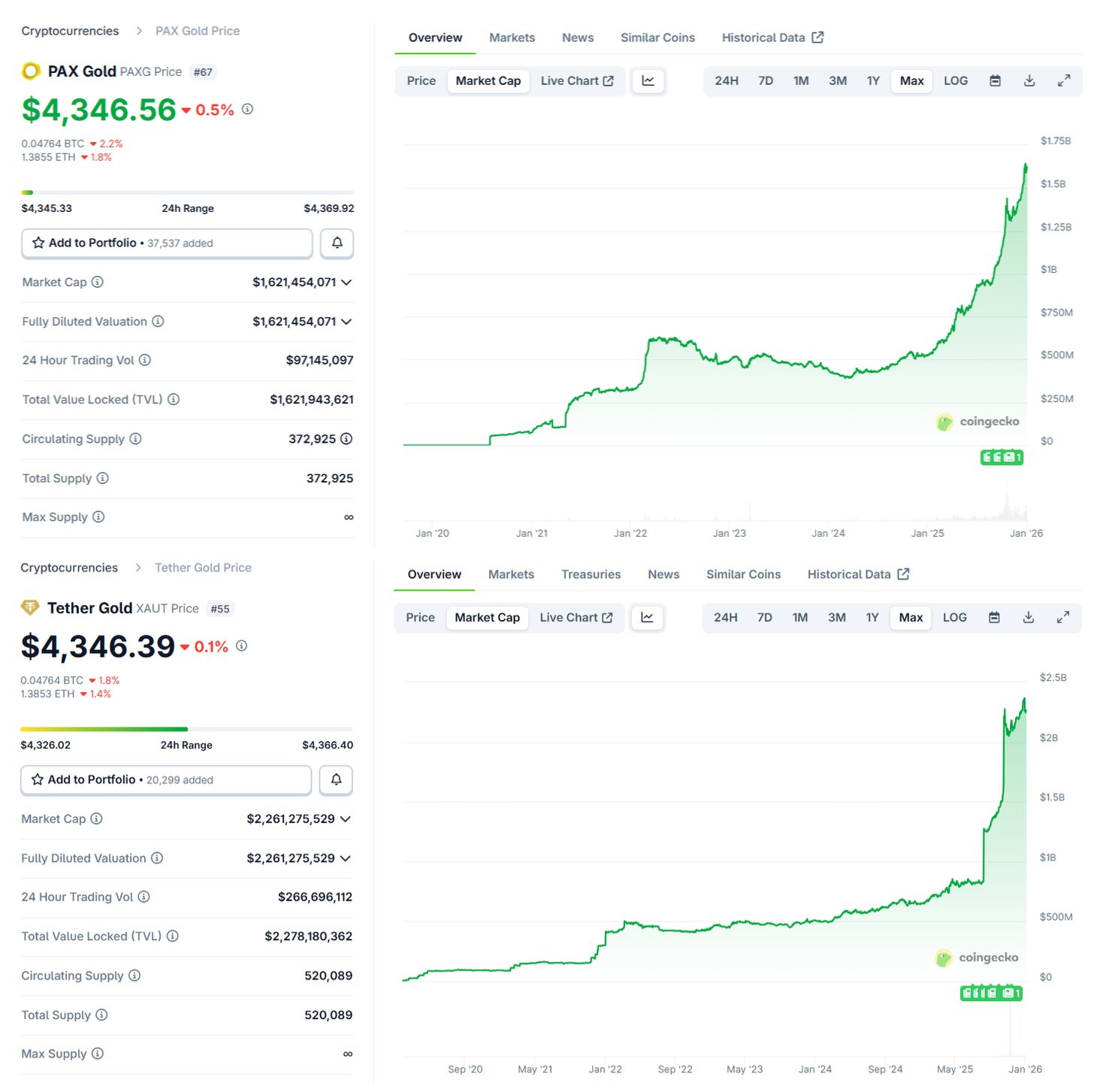

From a historical perspective, Paxos was one of the first issuers of gold-backed stablecoins with PAXG, where each unit in circulation represents the equivalent of one ounce of gold.

However, since 2025, Tether has established itself as the largest gold-pegged stablecoin, with more than $2 billion worth of gold currently in circulation.

We know that interest in gold is mainly due to its price, which rose sharply throughout 2025 (curiously, an asset reputed to be a store of value seems to be as volatile as stocks). The fact remains that the total market cap of onchain gold has exceeded $4 billion in just one year, just like this.

Then, silver followed gold in its relentless surge to such an extent that silver has reached a new all-time high. For now, the main silver-pegged stablecoin issuer is Kinesis with KAG. But considering how silver is performing recently, this would be a matter of time before so other issuers like Tether launch their onchain silver too.

Speaking of which, it's pretty surprising to see the absence of DeFi stablecoin issuers allowing to mint commodities (we can mint onchain stocks, so why not?)

Last words

To be honest, it's impossible to expect non-USD stablecoins to take significant dominance from USD. If they manage to get 5% of the total stablecoin supply, this would be a huge victory; it would be all the more impressive given the enormous network effects of the USD.

But while some governments are accelerating stablecoin frameworks, others use non-USD stables as a lifeline, non-USD stables start to harness DeFi, and commodities are coming onchain, there is still a large consensus telling "nobody wants non-USD stablecoins".

Of course we do.

Streaming payments

Instead of paying in one go, we pay continuously over a set period (instead of paying $100 in one go for a monthly subscription, we pay $0.00003 every second). This is what streaming payments are all about.

Streaming protocols have been in production for several years now, so this concept is far from new. That said, streaming payments enable options that no fintech can replicate outside of blockchain.

Streaming DCA

We talk a lot about Dollar Cost Averaging (DCA) in crypto, and streaming payments are definitely next-level DCA.Traditional DCA involves manual purchases regularly (e.g., weekly or monthly), but:

- Each purchase requires a separate transaction + associated gas fees

- How can we have a "regular basis" when transactions are made on our own discretion? Unforeseen circumstances, oversights and other unexpected events prevent us from being as regular as we claim to be.

The good news is that streaming DCA addresses both problems. Streaming DCA requires only one transaction to start the stream, after which the investment continues automatically without additional gas costs or manual interaction. In addition, tokens flow continuously from a sender to a receiver at a defined per-second rate.

Streaming Payrolls

Basically, payrolls rely on fixed monthly cycles. With streaming payrolls, salaries are converted into a per-second rate and sent to the worker's wallet in real time.

In other words, workers do not have to wait for a "payday" to start using their funds, and in case their funds are used for getting yield-bearing assets, they begin compounding interest the second they arrive in the wallet.

Streaming payrolls have advantages for organisations too:

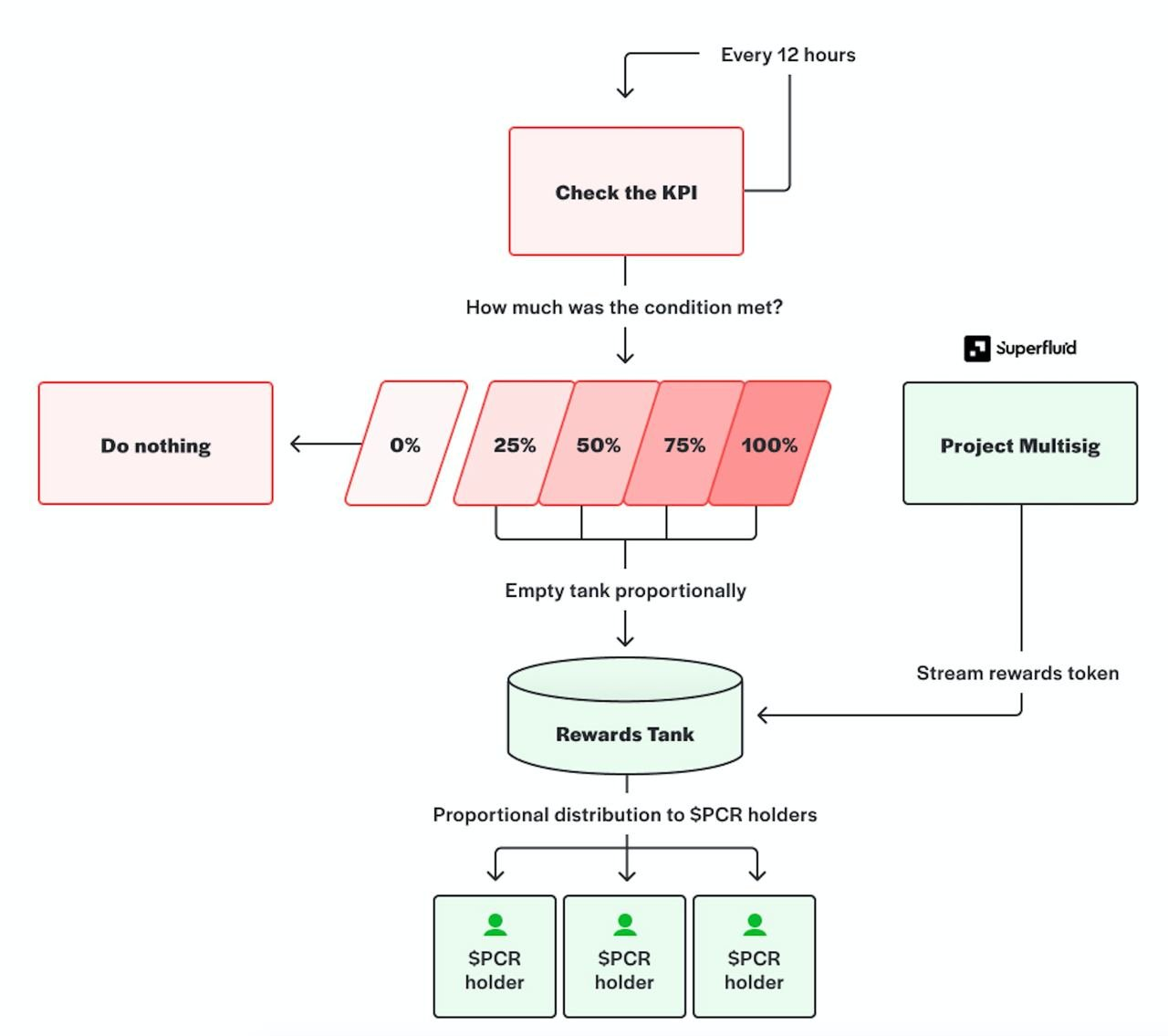

- Organisations can automate recurring payments, eliminating the need for monthly manual signing of transactions, especially for those involving a multisig.

- Organisations can set up "pay-as-you-work" models where they can cancel a stream immediately if a contributor fails to meet deliverables, protecting the treasury from bad actors

The "Pay-as-you-work" model can also apply to all kinds of commitments, including community incentives.

With this model, we have a way to reward members proportionally for contributing to given goals, and it is possible only thanks to streaming payroll.

Streaming Subscriptions

Here are the advantages of streaming payments for subscriptions:

- For customers, it gives more control as they can set a predetermined termination date, or start/stop the flow as they want

- Merchants can monitor the stream in real-time and do not have to wait until the end of a billing cycle to see if a payment fails

- Streaming enables the viability of micro-payments, where payments are too small to be economical in traditional banking systems. This is particularly transformative for content of any sort, where users can pay for content precisely.

Boosted compound effect

Streaming payments allow for increasing the compounding frequency to a point where it can be considered as continuous compounding. This allows for getting higher yields with yield-bearing assets.

For an annual interest rate r compounded n times per year, the classic formula is: A=P(1+r/n)^nt

- P = Principal

- r = annual rate

- t = time in years

- n = compounding frequency

With continuous compounding, n tends towards infinity.

lim(n→∞)(1+r/n)^nt=e^rt

So we get A = Pe^(rt) with continuous compounding, meaning that we transition from power scaling to exponential scaling, which is more powerful.

Of course, it is impossible to reach exponential scaling with streaming payments in practice, as transactions remain discrete (albeit numerous).But in the end, we come out ahead for two reasons:

- For investing $1,000 at 10% annual interest for 1 year, we still get more with an Ethereum block basis (+$5.17) than a monthly basis (+$4.71)

- Compound effect can't be cancelled by transaction fees, as we only need one transaction for the stream, whereas periodic purchases involve transaction fees each time

Some names

- Superfluid

- Sablier

- LlamaPay

- Nerite, powered by Superfluid

With these four names, we already have a good overview of what is happening in streaming payments.

It is somewhat unfortunate that crypto is not used enough for payments, but here we have a real primitive that TradFi cannot replicate.

Onchain office

Think of Microsoft Office or Google Suite, but onchain...That's it!

No matter what we do, we end up writing documents or creating Excel spreadsheets that contain information of a more or less sensitive nature.

However, the more we learn about how Microsoft Office and Google Suite work, the less we want to keep files in them, especially when we need to keep information that only we should know.

The problems

When using Office/Google Suite, our data is stored on their servers. This simple fact already causes many problems:

Data ownership is "trust me bro". Because documents are stored on corporate servers, the provider retains physical control and the keys to the data

Offline brittleness. Google Workspace often prevents users from writing if their Wi-Fi is patchy or disconnected, as if the software was designed to constantly "talk" to a server for data collection rather than leveraging the significant local computational power of the user's own device

Censorship risks. Because these platforms act as central authorities, automated moderation algorithms can block access to data or delete accounts entirely without notice

Systemic outages. On 29th October 2025, Azure experienced a global outage triggered by a configuration change in Azure Front Door that disrupted many Microsoft services, including Microsoft 365.

Not to mention the data leaks, and other fun stuff as Google Dorking queries 👇

Google Drive :) huh

— Frey (@offsecrunner) January 25, 2025

site:https://t.co/z0vbiya4ai inurl:folder

site:https://t.co/z0vbiya4ai inurl:open

site:https://t.co/onC2uL9NmZ inurl:d

site:https://t.co/z0vbiya4ai "confidential"

site:https://t.co/onC2uL9NmZ inurl:d filetype:docxhttps://t.co/cKy7myymj3

For context, this is a report detailing a critical vulnerability where a U.S. Department of Defense Google Drive exposed military orders and operational details. Fun.

More problems with AI

Alongside all this, there is also the fact that data is used to train AI models.

Google’s terms of service allow Docs data to be used to “improve services,” which could potentially include AI systems like Gemini. This means your documents may be exposed in several ways:

- Training and tuning: Your writing may be used to inform and refine Google’s language models

- Metadata logging: Who you collaborate with, when, and how long you write is collected

- Search and indexing: Even files marked ‘private’ are processed and indexed by Google, making them easier to surface for features like search, suggestions, and possibly AI tools

This is a word-for-word copy-paste of that article, and it was worth sharing here.

As for Microsoft, it seems to be taking the same path as well. Word automatically saves new documents to its OneDrive cloud service instead of leaving the default local backup.

This switch is part of the integration strategy for Copilot, Microsoft's AI, which requires cloud access to files. This change could occur across the entire Microsoft Office suite, including Excel.

The solution with Fileverse

To sum it up in one sentence, Fileverse is a privacy-first productivity suite. At a time when onchain privacy is becoming a growing concern, off-chain data privacy also has its importance. Fileverse has a total of 4 core features:

- Ownership. Instead of storing files on corporate servers, users deploy their own smart contracts (called "Portals") that act as private registries for their content

- End-to-end encryption. Documents are encrypted on the user's device before being uploaded, so the platform literally cannot read the content or use it to train AI models

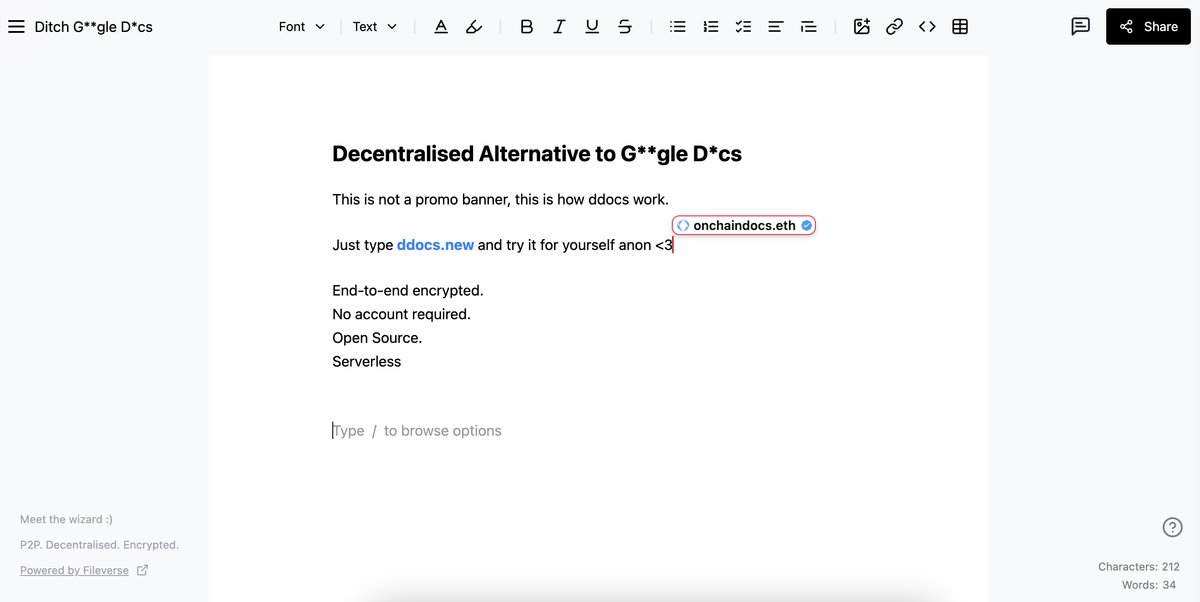

- Accessiblity. Users can start writing or collaborating instantly via ddocs.new and dsheets.new without a signup or email, and can sign up with their wallet

- Decentralization. Fileverse utilises a decentralized stack (IPFS, Arweave, Ethereum, WebRTC) to pass the "Walk Away" test: even if the Fileverse team disbands, the documents and workspaces remain operational

Now that the picture is clear, let's take a look at Fileverse's products, starting with ddocs.new.

ddocs is the equivalent of Google Docs / Word. Anyone can create or import some docs, and it supports both async and real-time collaboration.

It is also possible to create slides with ddocs, as it has Markdown & LaTeX compatibility.

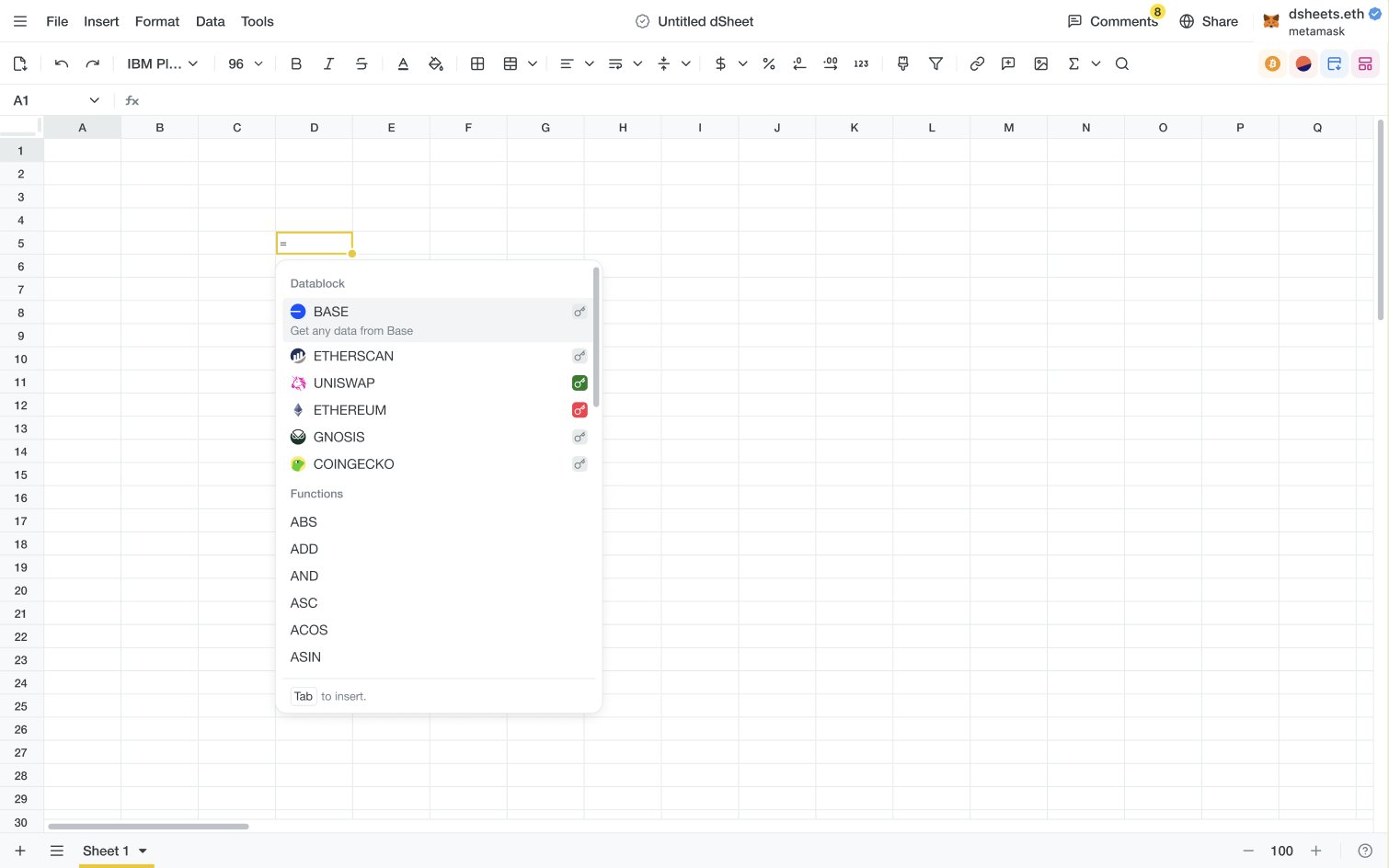

The second one is dSheets, the equivalent of Google Sheets / Excel. And apart from creating sheets like we usually do, the most interesting thing about dSheets is the "onchain functions".

Onchain functions can be used when we type formulas like =EOA, =COINGECKO or =DEFILLAMA in the cells, so we can pull live onchain data from some blockchains (Ethereum, Base and Gnosis so far) and compare stats.

All of this allows us to query, manipulate, and write onchain data using spreadsheet logic (which may represent an alternative to Dune, but it's not a competition).

One more cool thing is the possibility to share "public community dSheets", so we can see what the possibilities with it are.

d/acc + privacy in prod

Fileverse has done something big: create something combining decentralization and privacy, and it works.

The best part is, Fileverse's proposal has nothing to do with speculation. It is a use case that is of interest to anyone who uses office software daily.

Of course, Fileverse has fewer features than other Suites, and there is room for improvement, but we can keep in mind that the team bring upgrades regularly.

I've been impressed by @fileverse (decentralized open-source encrypted docs https://t.co/WXjBwytG5V ). Every month more bugs get fixed, and recently it's finally at the point where I can comfortably send docs off for comment or collaboration, and things reliably don't break.

— vitalik.eth (@VitalikButerin) December 10, 2025

We all know crypto and DeFi deserve better than Google or Microsoft, that's why I'm a regular user of Fileverse, which is already leading the onchain office narrative