Fees overview in decentralized exchanges

We only look at swap fees in a decentralized exchange, but there are multiple fees to take into account

In most cases, when we look at decentralized exchanges (DEX) fees, we only look at swap fees, i.e. the fees charged by the liquidity pool.

However, there are multiple fees to take into account, and for some time now, the dynamics of DEX fees have been changing.

Let's do a quick overview about DEX fees, and my theses about how they will evolve :

1️⃣Swap Fees

- 🦄 Uniswap v3 charges 0.01%-1% swap fees

- 📈 Maverick charges 0.002%-3%

- 👨🌾 Trader Joe charges 0.01%-0.8% + dynamic fees

The more volatile the exchange pair, the higher the swap fees can be expected on the pair. These fees are mainly used to pay liquidity providers for their service

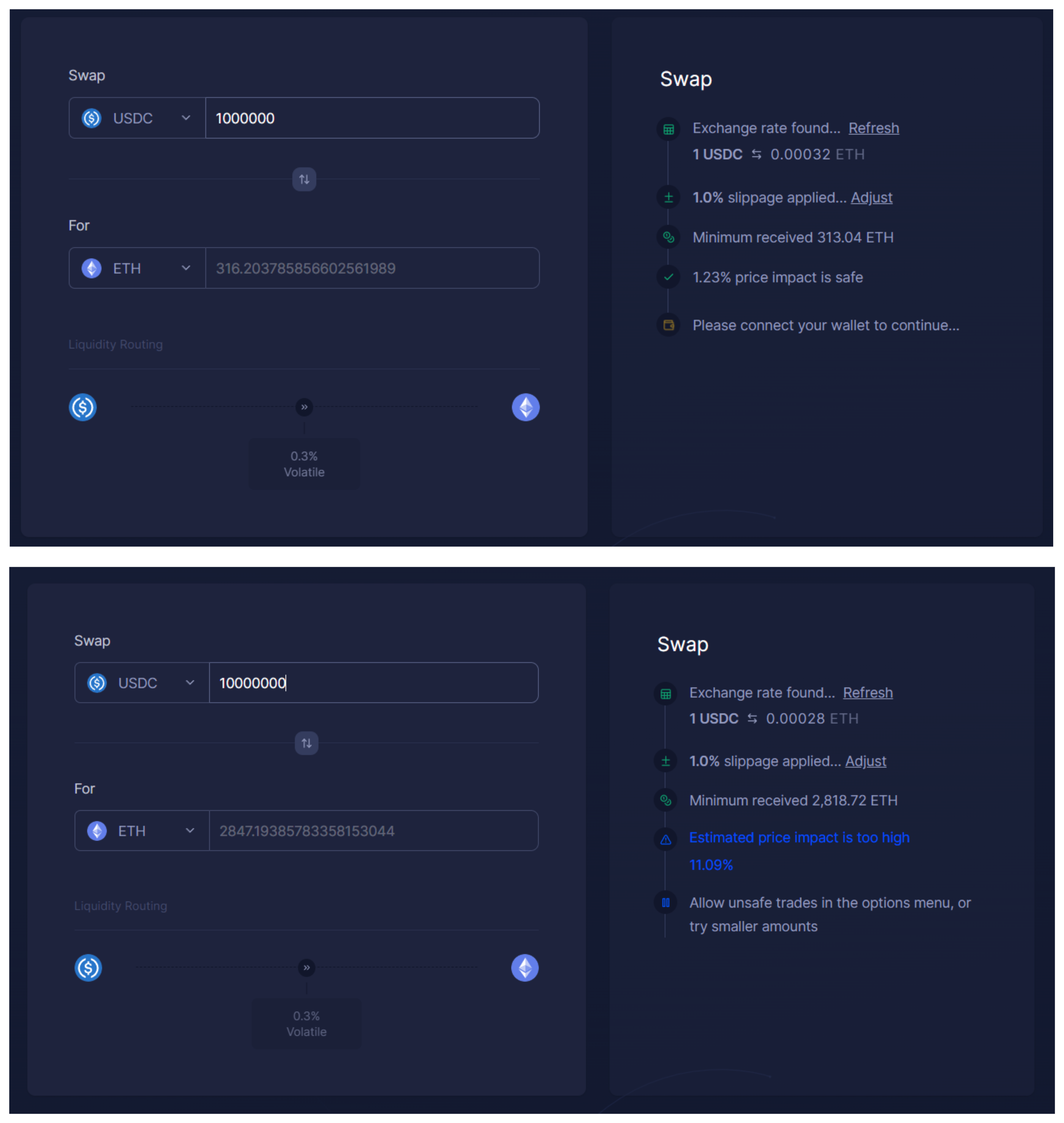

2️⃣Price Impact

Technically, an AMM will always allow users to trade, regardless of the liquidity of the crypto involved.

But when the transaction becomes too large for the available liquidity, the missing liquidity is paid by the user.

Example with Aerodrome's ETH/USDC pair :

😀For $1 million traded, we have $985,000 on arrival

😒For $10 millions traded, we have $8.891 millions

3️⃣Slippage

Slippage (not to be confused with price impact) is the unpredictable price evolution from one block to the next.

A DEX uses an algorithm to update the swap price between two tokens. But this algorithm can only update the price with each new block.

Imagine a car that indicates its speed every 12 seconds...That's how DeFi feels like on Ethereum

Since prices are updated periodically and not in real time, we can expect unpredictable price changes, both positive and negative :

In case of negative slippage, the user receives less than expected.

In case of positive slippage, there are two possible situations :

- The user keeps the difference and earns a profit

- Protocols keep the difference. Usually, it's the DEX aggregators that do it (Kyberswap, Paraswap, 1inch discontinued it in 2023), and this is an invisible cost to the user.

4️⃣Frontend fees

To use blockchain, the vast majority of users use a web interface. But using a web interface can expose us to additional costs:

We pay 0.875% on each trade for using Metamask's swap feature

We pay 0.25% on each trade for using Uniswap's interface (it was 0.15% at the start, but has since increased).

How those fees would evolve

So we have swap fees, price impact, slippage and frontend fees to consider when we use a decentralized exchange.

Now we can wonder if those fees will go up or go down in the future. Here are my (very personal) takes :

Swap fees will go down. Swap fees and liquidity provider (LP) yields are communicating vessels : the higher are the LP yields, the lower are the swap fees (as long as there is no monopoly)

LP yields depend on the liquidity structure (x*y=k, Stableswap...) and the incentive model (e.g. ve(3,3) from Velo/Aerodrome) of the DEX. Since 2018, we've seen tremendous progress in both fields and this will probably continue to reduce swap fees.

Price impact will go down. Today we see lots of different liquidity structures for almost all kind of swaps :

- x*y=k (Uniswap) for volatile assets

- Stableswap (Curve) for stablecoins

- Dynamic distribution (Maverick) for liquid staking tokens or liquid wrappers

- Time-Weighted Average Price (TWAP) orders for big trades

- and others...

Not to mention we have aggregators to combine all this. Just like swap fees, research and competition will bring price impact down.

Slippage will stay as it is for a while. DeFi is very volatile by design, and despite the fact that it is more efficient than traditionnal finance as a whole, there's still a long way to go before DeFi is institutionalized and therefore reduce slippage.

Frontend fees will go up. We've seen it with Uniswap, they're not afraid about raising frontend fees because they know most users will use the frontend anyway, and this is confirmed by Metamask, which made $280 million with the swap feature

Of course, those frontend fees can be mitigated, just like this dev who noticed that Uniswap hosts historical versions of their interface, and found a version which contains 0 fees. But unless being savvy, this is difficult to escape this and I wouldn't be surprized to see frontend fees as the primary revenue for DEX builders.

The "Coincidence of Wants" Case

Example : An owner of a property and a tenant both use an intermediary like Airbnb to match supply and demand.

The problem is that the fees imposed by the platform penalize both the owner and the tenant. So they can agree on a cash exchange without going through Airbnb :

- The tenant pays less for the same service

- The owner earns more by bypassing commissions and taxes

Coincidence of Wants ("CoW") makes exchange more efficient for stakeholders.

As long as there are liquidity pools, there will be CoW. And the more pools there are, the more relevant CoW will be.

If we apply this for decentralized exchanges, we have CoWswap :

In the worst-case scenario, the value we obtain is equivalent to what we would have in a classic aggregator, so nothing is lost

Otherwise, a CoW is found between the buyer and seller, and both earn more :

- No swap fees

- No price impact, as they operate outside of liquidity pools

- No MEV attacks (frontrun, backrun, sandwich attack...)

CoWswap has first mover advantage in this field, but competition already intensified with 1inch (Fusion), Uniswap (UniswapX) or even Paraswap (upcoming Portikus) who joined the melee.

Why bringing up CoW Protocols to talk about DEX fees ? Simply because CoW protocols are a good representation about how DEX fees would evolve :

- They involve no swap fees

- They involve no price impact

- Altough they protect from MEV attacks, slippage will not change

- They have a specific infrastructure that must be profitable, so they have frontend fees.

And all this corresponds fairly well to my personal theses quoted above, but they can be wrong as well. The DeFi landscape evolved deeply during the last 5 years after all.

Your opinion matters : How do you think the DEX fees will evolve in the coming years ?